QUESTION 1

On 1 January 20X6 Stremans Co borrowed $1.5m to finance the

production of two assets, both of which were expected to take a year to build.

Work started during 20X6. The loan facility was drawn down and incurred on 1

January 20X6, and was utilised as follows, with the remaining funds invested

temporarily.

Asset A Asset

B

$'000 $'000

1 January 20X6 250 500

1 July 20X6 250 500

The loan rate was 9% and Stremans Co can invest surplus funds at

7%.

Required

Ignoring compound interest, calculate the borrowing costs which

may be capitalised for each of the assets and consequently the cost of each

asset as at 31 December 20X6.

QUESTION 2

Acruni Co had the following loans in place at the beginning and

end of 20X6.

1 January 31

December

20X6 20X6

$m $m

10% Bank loan repayable 20X8 120 120

9.5% Bank loan repayable 20X9 80 80

8.9% debenture repayable 20X7 – 150

The 8.9% debenture was issued to fund the construction of a

qualifying asset (a piece of mining equipment), construction of which began on

1 July 20X6.

On 1 January 20X6, Acruni Co began construction of a qualifying

asset, a piece of machinery for a hydroelectric plant, using existing

borrowings. Expenditure drawn down for the construction was: $30m on 1 January

20X6, $20m on 1 October 20X6.

Required

Calculate the borrowing costs that can be capitalised.

Answer

Question 3

An entity already has a number of general loan arrangements:

Loan 1 of $800,000, interest paid at 9%;

Loan 2 of $2 million, interest paid at 8%; and

Loan 3 of $400,000, interest paid at 7.5%.

The entity has commissioned a new printing press to be constructed

on its behalf. The total cost will be $800,000 and the entity will be able to

fund the purchase from its existing borrowings since it has arranged for stage

payments to be made. The construction takes six months.

Required

Calculate the borrowing costs that can be capitalised and the

total cost of the printing press.

Question 4

An entity borrowed $5 million to fund the construction of a new

building. Interest is payable on the loan at 8%. Stage payments were due

throughout the construction period and therefore excess funds were reinvested

during that period. By the end of the project investment income of $150,000 had

been earned and the construction took twelve months to complete.

Required

Calculate the borrowing costs that can be capitalised

and the total cost of the building.

Question 5

The following events take place:

An entity buys some land on 1 December.

Planning permission is obtained on 31 January.

Payment for the land is deferred until 1 February.

The entity takes out a loan to cover the cost of the land and

the construction of the building commenced on 1 February.

Due to adverse weather conditions there is a delay in starting

the building work for six weeks and work does not commence until 15 March.

Required

What date should capitalisation of borrowing cost commenced?

In the above scenario the key dates

are:

Expenditure on the acquisition is

incurred on 1 February when construction commences.

Borrowing costs start to be

incurred from 1 February.

Although work was being

undertaken on planning permission etc. during December and January, no

borrowing costs were incurred during this period.

During the six-week inactive

period borrowing costs should not be capitalised.

Capitalisation of borrowing costs

should commence from 15 March.

Question 6

Concorde Inc. obtained a term loan during the year ended December

31, 2008, amounting to $650 million for modernization and development of its

factory. During the year, buildings costing $120 million were completed and

plant and machinery amounting to $350 million were installed.

A sum of $70 million has been given as a capital commitments

advance for assets, the installation of which is expected in the following

year. The amount of $110 million has been utilized for working capital

requirements.

Interest incurred on the loan of $650 million during the year

ended December 31, 2008, amounted to $58.5 million.

Required

How should the interest amount of $58.5 million be treated in the

financial statements of XYZ Inc.?

Interest

incurred amounting to $58.5 million should be apportioned using the amounts of

loan utilized for various purposes. Except for the portion of the loan that was

used for working capital requirements ($110 million), the rest was utilized for

the construction of qualifying assets, and therefore the borrowing costs

eligible for capitalization will be

$(650 – 110)/650 × 58.5 million = $48.6

million.

Question 7

Funto Construction has three sources of borrowings:

Average Loan Interest

Expenses

N N

7 Years Loan 8,000,000

800,000

10 Years Loan 10,000,000 900,000

Bank Overdraft 10,000,000 900,000

The 7 year loan has been specifically raised to fund the building

of a qualifying assets.

The company has incurred the following expenditure on a project

funded from general borrowings for the year 31st December 2014:

Date

Incurred Amount

N

31st

March 1,000,000

31st

July 1,200,000

30th

October 800,000

Required

Determine the weighted average and the amount that will be

capitalised.

Question 8

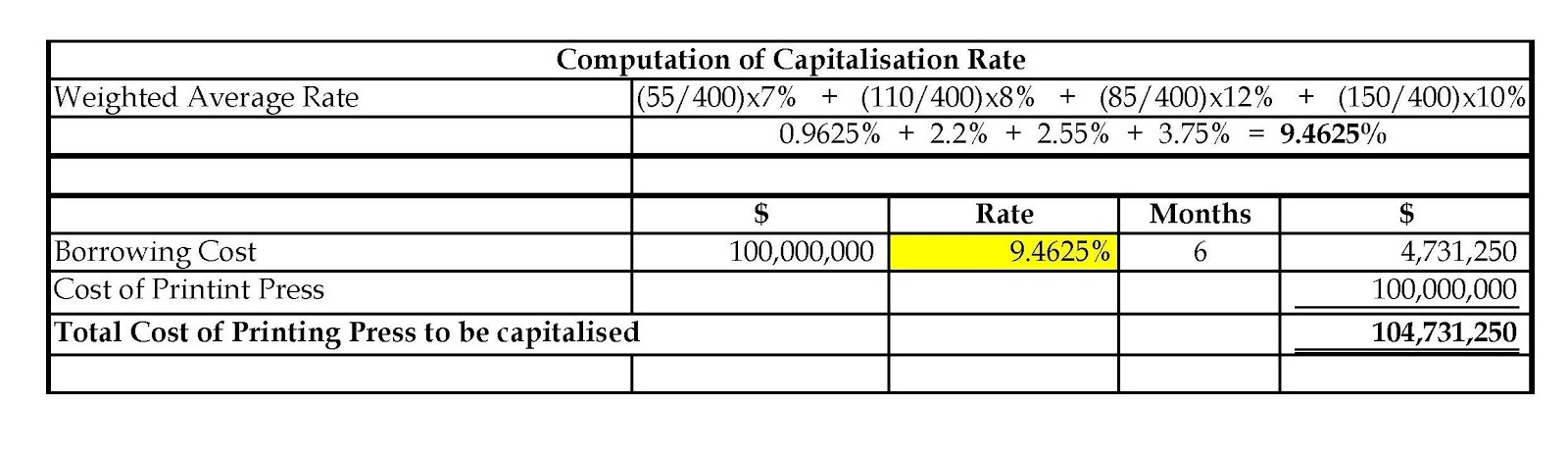

Lala Plc, a geared company has the following loan arrangements as

at 1st January 2011:

Average Loan

N

7%Loan notes 55,000,000

8% Loan notes 110,000,000

12% Debentures

85,000,000

10% Bank Loan 150,000,000

On the 1st of January 2011, the company commenced the

construction of a new office factory. The construction of the factory will cost

N100,000,000 and the company funded the construction with the existing

borrowings. The factory was completed on 31st August 2011 but was

not available for use until 1st December 2011 as a result of minor

modification. During the construction period, active work was interrupted and

the building construction was stopped for two months as a result of adverse

weather conditions.

Required

Calculate the borrowing cost to be capitalised and the cost of the

building to be recognised upon initial recognition.